How to solve 93.6% of your investment problems using one question.

The questions an investor (or his/her advisor) asks, determines how well their investments grow. Better questions equals better returns.

Unfortunately for investors (and their advisors) many are asking the wrong questions.

They’re asking questions about diversification. And age. And self-described risk tolerance. These are the wrong questions to be asking today.

And that’s why most people’s investments are suffering. It’s not because of the Fed, politics or the economy. But their questions.

But it doesn’t have to be this way.

Because as people get older, years become seasons and then months and weeks.

Knowing how to avoid the large debilitating losses can be the difference between a future of stability and growth or a future of angst.

Are you even asking the right investment questions? What if you weren’t? What if you were asking questions that stopped being relevant 20 years ago?

In addition, what if there was one question that was also able to filter out all the hype and fear-mongering thrown at you by the “pick of the month” newsletter world and money channels?

What if there was one question that clearly showed you the world of Big-Box Advisors were hurting you more than you even realized?

I’m asking because there’s one question above all others that matters most to an investors growth and stability.

This question determines 93.6% of a person’s investment performance. And if you get the answer to this question right, you get everything right. BUT if you get it wrong then it doesn’t matter what individual stocks or sectors you own.

But before I get to the question which solves 93.6% of all of your investment issues and answer (which I will), you first have to understand what world your money is in because it matters.

Which world is your money in?

The Big-Box Advisor World. This world has an investor “buying and holding”- this is a world where the investor rides out the hard times and takes the full hit of every market correction. And whether that investor is all in stocks or is in a 60/40 stock-bond split, they are taking on unnecessary losses.

Or is your money in this world?

The“Pick-of-the-month” Newsletter World. This world has an investor buying, trading and chasing stories for the next big thing. This world wants the investor taking actions (more trading) by following great stories. And whether that investor is old or young, this world values activity and stories over stability and safety.

Here’s a sad but true fact…

Almost all of investors have their money in one of these two worlds so it makes sense how an investor could think they only have two choices.

What most investors don’t know is that there is a third choice. A choice that’s NOT based on buy-and-hold or trading/buying stories.

How does an investor filter out the noise, hype and fear? And know what really matters…

The third choice takes the best part from the Big-Box World and the Pick of the Month Newsletter World. What are those best parts?

Big-box advisor are almost always “buy and holder.” It’s this behavior that is important 78% of the time. And the Pick of the Month Newsletter World is right that losses have to be managed and that being active is important.

So how does an investor use the best of “buy and hold” and the best of “active?” In other words how do they know when to “hold’em” and when to “fold’em?”

They use what we call The Rosetta Stone of Investing.

If you don’t know, the Rosetta Stone was the key to deciphering hieroglyphics in the last part of the eighteenth century. And before the discovery of that stone (1799) the world had no way of understanding hieroglyphics.

Why does understanding hieroglyphics matter in the framework of investing?

Because hieroglyphics are what most investors experience is, in understand what really works in investing.

Both the Big-Box World and the Pick of the Month Newsletter World told investors they knew how to decipher investment hieroglyphics with their own “stone”…

Is your money in the Big-Box Advisor World that believes “buy and hold” is key?

Most investors just kind of end up in the Big-Box World. It’s where the masses move first. But investors don’t know why they are here – it’s just what everyone else is doing.

And yet some of are starting to notice, no one is really happy here. They’re just sort of resigned that this is all there is.

How do you know if your money is in the Big-Box Advisor world?

This is actually an important question as most people “trust and like” their advisor and think their “Guy” is different. Is he? She?

So how do you know?

-

- Did your money stay in the market for the ‘00 and/or ‘08 market crash?

-

- Is your money in 10 or more investment positions?

- Is your money allocated based on your age and self-described risk tolerance?

If you said yes to two of the three statements, then your money is almost certainly sitting in the Big-Box Advisor world and taking unnecessary risks.

Or is your money in the Pick-of-the-Month Newsletter World, which believes activity (great stories and the next Facebook of “fill in the blank”) is the answer?

The Pick of the Month Newsletter world believes the best choice for you is to have 30 even 40 ticker symbols in your portfolio with new symbols being exchanged in and out each month (read: activity).

This world can feel better.

A feeling of “my type of people.” And, now at least I’m doing something about it. People can find critical thinkers, and people getting mad at the government and Wall Street can find a place here. These are the Do It Yourselfers (DIY).

Still, it’s not relaxing or calming. In fact it’s even more stressful than the Big-Box World.

How do you know if your money is in The Pick of the Month Newsletter World?

- If you’ve been too conservative for years because of an imminent crash that never came.

- If you subscribe to three or more investment newsletters.

- If your inbox is overflowing with stories about the next “facebook” of…

If you identify with two of the three above then your money might possibly be in the “Pick-of-the-month” Newsletter world.

And the worst part, the “Pick-of-the-month” newsletter world dumps so much hype, fear and overwhelm on their investors that they are left with angst and poor performance.

The most glaring problem with the Big-Box Advisors and the Pick of the Month Newsletter world is they both teach their own version of investment hieroglyphics (read: confusion, complexity and complication).

Though both worlds claim to be polar opposites of each other they’re actually teaching the exact same thing, namely…

… “Investing is complex and the solution is complicated too, but we’ve got your back with our complicated solution.”

But it doesn’t have to be this way. The investor doesn’t need to live in a world of angst or worry. The investor doesn’t need to be passive OR active. Trading OR “buy-and-holding”.

There’s a third choice.

A choice WITHOUT complexity, fear, hype, confusion and outdated ideas from the 1970’s.

Do you know you have a third choice? A choice that is based on a powerfully simple approach?

This world is harder to find in the world of hype and fear.

It’s a bit secluded — away from the noise and drama of the Big-Box World and the “Pick-of-the-Month” Newsletter World. In fact, this third world has been described as relaxing even.

It actually takes a little getting used to. The first night is strange because there’s very little noise… no stirring around, no sirens, no yelling, no hyping…. just calm.

The third world is different.

The language is weird. Weird in a simple sort of way. There’s no jargon used. The third world notices the obvious. No hieroglyphics. Not even many words, mostly pictures and images that are obvious and clear to you.

This world can be very off-putting to refugees of the Big-Box Advisor World and Pick-of-the-month newsletter World at first.

Some people are starting to notice they are interested in a different way. A way where they don’t take the full hit of the big market corrections? A way where they are not inundated with hype or fear.

For those that are interested. An investor can get clarity, stability and growth in four steps.

[optin-monster-shortcode id=”vy9oeustpcet8zy1u1bv”]

STEP #1:

THE ASSET MATTERS MORE THAN ANYTHING ELSE.

Every investor only has four investment choices on this planet: stocks, fixed income (bonds/cash), commodities and real estate. That’s it. Four. Not 44. Or 444. Or 4,444. Four.

And if you get the asset class right you get 93.6% of everything you have to get right to create stability, growth and certainty.

You can read about the study that clearly proved asset allocation matters most here, here and here.

If you do follow those links you will notice the numbers actually range from 91.5% all the way up to 100%. It all depends on how the reader interprets the data.

Vanguard, yes that Vanguard said, in the third link just above that given all factors… assets really account for 100% of the variation in performance.

The right asset, is where you win or lose.

AND not with the sector or individual company. Get the asset class right and you get [almost] everything right.

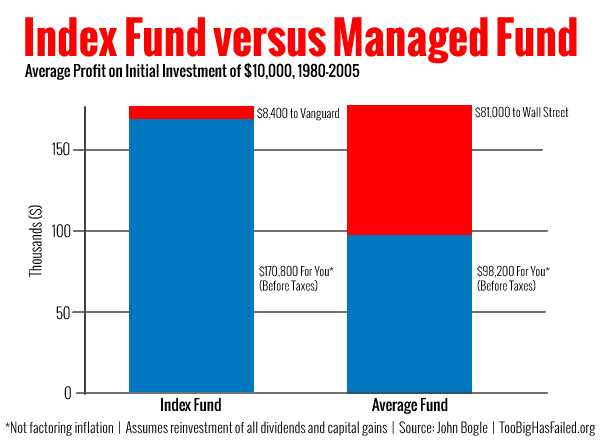

Stocks beat the other three assets 78% of the time

Out of the four asset classes, stocks lead the other three assets higher 78% of the time. And if the investor reinvests their dividends when buying a simple stock index fund they immediately move themselves to the front of the performance line. AND makes it even that much harder for the other three assets to compete.

Look below and see how this one powerfully simple step can change an investor’s life.

The blue stack of returns is where the investor wants to start the conversation. Not end it. Not forget about it. But start the conversation.

The key is its simplicity. You only need to decide between four assets. And if you set real estate aside because real estate is either a house or land or an apartment building and not a ticker symbol that you move in and out of, you are down to three assets (stocks, fixed income and commodities).

And if you want to make it even easier, you can drop commodities as they tend to have higher price volatility then even stocks.

And now you are down to two choices. TWO!!!

STEP #2:

STOP DIVERSIFYING IMMEDIATELY

Everywhere. And I do mean everywhere. You are told to diversify.

The problem is even IF you get the sector or stock right it only adds 2% to what you need to get right. And remember getting the asset class right determine 93.6% of what you need to get right.

Also, when the stock market falls hard (read: more than 10%) all stocks, sectors, slices, segments and sizes fall hard too. The world is interconnected and information is immediate today. And large drops affect everything today.

Take a look at the 2008 to 2009 Global Financial Crises for example. The S&P500 fell 58% from top to bottom.

And there was nowhere to hide in the stock market.

Not in domestics stocks.

Not in value stocks.

Not in dividends stocks.

Not in international stocks.

And not in different sized stocks (small, medium or large).

If an asset is going to get crushed. It’s taking everything with it inside that asset. This is true for stocks, bonds, cash, commodities and real estate.

The direction of the asset class matters most. More than anything else. This is more important than your age and even your self described risk tolerance.

Now, if an asset is only going to fall 10% then it still doesn’t matter to be diversified. Because part of your money will be underperforming the core asset and parts of your money will be outperform that same core asset. And what you’ll end up with is the assets over all return. But with lower numbers because of unnecessary fees and commissions.

The idea that owning 30 different stock symbols that are falling together is safer than just owning the market is old thinking. And is expensive.

If an investor owns more than six ETFs or 20 stocks… then they own the market. And when the stock market falls hard. All stocks fall with it. Period. The same goes for all four asset classes.

If the above asset class ship hits an iceberg, it doesn’t matter where your money is on the boat.

STEP #3:

KNOW WHICH ASSET IS STRONGEST

Which of the four asset classes is trending higher absolutely and relative to the other three asset classes? This is the question all investors want to be asking and answering.

And this answer tells you where the stability is.

If the investor knows how to get this answer they know where the stability is in the investment world. They know where new money is flowing. They know how to protect their downside and participate in the upside.

In other words, they know almost everything thing they need to know about where when and how to invest.

And look 78% of the time the stock asset class will be beating the other three both in absolute terms and in relative performance.

But what to do about that other 22% of the time?

That 22% is short on time, but can be long on devastation.

Especially if the investor considers that some of the drops in that 22% of time can be 50%, 60% and even 70% in size.

Yes the market always comes back. But sometimes “coming back” can take years and even decades. And as people get older, years become seasons and then months and weeks. That might be okay if you’re 35 but not if you are 55… or older.

An investor’s stability, steadiness, and freedom is directly connected to avoiding those large catastrophic asset class losses.

One of the keys to investing is NOT finding the huge wins. BUT avoiding big losses. This is what step #3 is about.

Let me show you what I mean.

Almost no one can beat the S&P500 with dividends reinvested…

Below is a price chart that compares a “buy-and-hold” approach with dividends reinvested (S&P500 w/ dividends reinvested).

Please note that 99% of investors cannot beat this index with dividends reinvested over any five year period. The red line in the price chart below is using this almost impossible-to-beat index that is free to buy, own and keep.

The blue line below is the result of asking one question AND knowing how to get its answer. That question again is: Which of the four asset classes is trending higher absolutely and relative to the other three asset classes?

To keep this example easy, the blue line only uses two investments.

Investment one is the same S&P500 w/dividends reinvested as with the red line (again no need to get complicated). And the second investment is the one-year US Treasury Bill. That’s it. Two assets: One is stocks. And one is short-term bonds.

Never be left holding the bag again.

Step three is having the investor ask the question, Which of the four asset classes is trending higher absolutely and relative to the other three asset classes? Or asked differently, “Is this the 78% of time to be in stocks…or is this that 22% to be out?

And when the investor knows where to find the answer to “in or out of stocks?” an investor’s life can change. Just look at the price chart below.

The red line is the S&P500 with dividends reinvested. Which by the way beats 99% of ALL investors over any 5-year period. Read that sentence again until it sinks in.

But look what happens when the investor asks one powerfully simple question. Again, the question is about avoiding the huge losses. That’s the blue line below and is the result of asking the “in or out of stocks” question.

Asking question #1 from January 1st 2000 until December 31st 2018 returned a 268% performance. That means $100k would have grown to $368k.

Where a buying and holding the S&P500 with dividends reinvested would have returned a 130% return over the same time period. That means $100k would have grown to $230k.

Notice there are two periods when the blue line almost goes flat?

That’s when Question #1 is getting its client’s money fully out of the stock asset class and putting them fully into the short-term bond asset class.

Why?

Because Question #1 is only concerned with knowing which asset is trending higher in price AND is also out performing the other three assets.

And those two flat periods is when this question got its followers fully out of stocks and fully into short-term bonds.

Two symbols. Less volatility. More stability.

SIDENOTE: Investing is not that simple. You’re a “timer.” And everybody knows “timing the market” doesn’t work. So shame on you RC.” And if this was so amazing why aren’t you a billionaire?

Who’s words are those?

What is the real downside risk to keeping an approach simple?

For many “simple” and “easy’ doesn’t work for people. This approach or thinking is not for everyone. It can trigger a lot of people.

Think about this.

Same politics. Same weather. Same Congress. Same Senate. Same President. Same inflation rate. Same FED. Same stock market. Same everything EXCEPT asking one question AND knowing how to get the answer.

Question #1 grows $100k to $268k in the same time that the almost impossible to beat S&P500 w/dividends reinvested grows $100k to $130k.

So, please take a giant step back and let me call out a few things.

Behavior Matters Most.

I’m not saying the investor would of have had the behavior chops to actually take action. I’m not saying the investor would have put all of his money in the index while the market was in that 78% stable uptrend.

I’m not saying the investor would have taken his money out of the market when question one said to get it out. And I’m not even saying the investor would have even taken any actions.

I’m not saying the investor wouldn’t have had to pay taxes when he moved his money from the S&P to US Gov’t Bonds.

I’m not saying investors wouldn’t have had fees.

There are many scenarios.

Though people can invest for free today (Robinhood). And 40% of all invested assets are in tax-sheltered accounts (IRAs, Roths, SEPs, 401(k)’s, Annuities.

And there were only two times in 17 years that the two questions had an investor’s money fully out of the market.

Plus an investor can buy the S&P500 index today for free.

The “One Question” vs. The S&P500 w/dividends price chart has two very large takeaways:

ONE: Question #1 didn’t try to beat the S&P500 with dividends reinvested, it joined it 78% of the time. And

TWO: All Question #1 did was avoid those rare but normal devastating losses.

My message is simple, There’s a better way.

It’s not passive. And it’s not active. It’s not buy and hold. And it’s not trading. It’s not timing and its not checking-out for 30 years. It’s not Big-Box. And it’s not “pick of the month” newsletter world.

It’s a third choice.

The pick of the month newsletter world has gotten it wrong for the investor. The answer is not in the 30 ticker symbols about the next “Facebook of China.”

And the answer is not looking at your age and self described risk tolerance and then buying and holding for the next 30 years.

The answer is in understanding what produce 93.6% of the variation in performance.

Growing money well doesn’t have to be anxious or difficult. But going it alone is exceptionally difficult.

STEP #4:

PARTNERSHIP MATTER

There’d be no HP without Hewlett and Packard. There’d be no Microsoft without Allen and Gates. There’d be no Apple without Jobs and Wozniak.

There’d be no Google without Page and Brin. There’d be no Ben & Jerry’s without… wait for it Ben Cohen and Jerry Greenfield.

There’d be no Beatles without McCartney and Lennon. There’d be no Stars Wars without Han Solo and Chewbacca.

You got to have the right partnership.

Working in splendid isolation is not how greatness happens.

Whether that’s music, business or ice cream. Finding the right partnership is part of the magic. It’s the one differences that makes the difference for greatness to happen.

The bridge to a better life is four powerfully simple steps put together.

If the investor takes all four steps he builds the bridge and gets to the other side of the river. The other side of the river already exists.

And it’s that side that the investor is looking for when they leave the long-only Big Box world and join the “pick of the month” world. But it wasn’t the investor’s fault.

No one had told them there was a powerfully simple way.

There’s a world where a Rosetta Stone is not needed (read: no hieroglyphics).

What investors want is economic stability.

And no one has told them its not found in narrative-based investment research. Or in the “age-based,” “buy and hold” world of Big-Box Advisors.

What the investor is looking for is “elegant simplicity” the type of simplicity you get after someone has gone through the chaos, confusion and complexity.

And when the investor is able to step above the noise and say, there must be a better way, they start to find themselves looking for the bridge to the other side. A side with almost no noise pollution.

Take the steps and see what world three can do for your life. The entire goal of world three with that one powerfully simple questions is to align your money to the the best asset class, regardless of age or self-described risk tolerance.

I know. I know. The Big-Box world wants you to believe you are the center of all your investment choices. Yes, it’s your money. And yes, your emotions have put you at the center of all stock market correction.

But if get your money to the asset that is in an absolute uptrend and is also outperforming the other three. Then…

…You get HP. Microsoft. Ben & Jerry’s. Apple. Google. Star Wars. And the Beatles.

If you’d like the map to world #3 you can find it here.

In Your Corner,

RC Peck, CFP

{kind=link}

Leave A Response

You must be logged in to post a comment.